Milan – October 15th, 2021

On October 15th, the annual event of the Component Manufacturers chapter of the Italian Association of Plant Engineering (ANIMP) took place in Milano, with the active participation of SupplHi. The annual event was held in presence with the attendance of about 150 professionals from the Plant Engineering industry

SupplHi presented the 100-page Energy Industry Global Markets Forecast and Supply Chain Trends 2021, developed in collaboration with leading international EPC Contractors.

The presentation was delivered by Mr. Daslav Brkic, Business Development Consultant, and by Mr. Giacomo Franchini, Director of SupplHi, followed by the annual roundtable with Business Development and Sales Managers of leading Contractors.

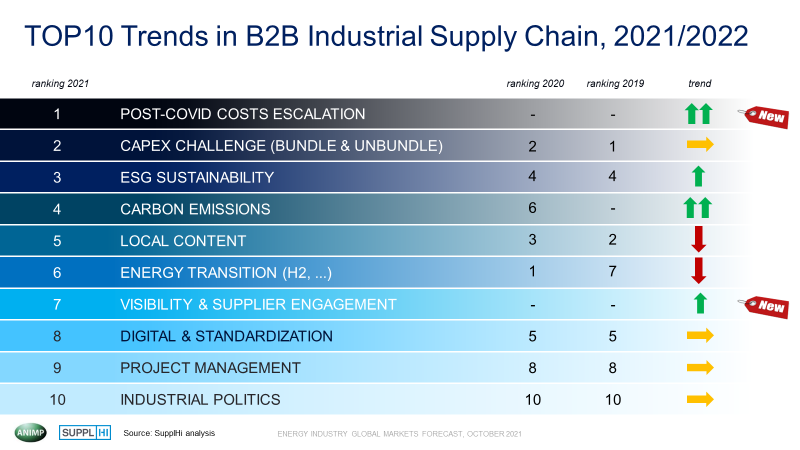

The Report included the traditional analysis of the Top 10 Trends in Industrial B2B Supply Chain. The industry is facing several priorities – some of them remain unchanged with respect to previous years – while others are emerging for the first time such as the Post-Covid Cost Escalation of commodities and the need for enhanced Visibility and Engagement of Suppliers. The focus on ESG and Sustainability is increasing with particular attention to the assessment, off-setting and reduction of Carbon Emissions.

We present below a summary of the TOP 10 trends in B2B Industry Supply Chain for the two-year period 2021/2022:

1. Post-Covid Costs Escalation: The market of commodities experienced an increase in prices and both supply and demand are being hit by a series of short-term shocks that are interacting in unpredictable ways. The cost for all critical equipment adjusted accordingly: steel structures in the range of +20% / +25%, low voltage cables in the range of +55% / +65% and so on. The question on how to manage a prolonged price escalation becomes now crucial for the industry.

2. CAPEX Challenge: What the market can pay to support new projects remains one of the main priorities. Contractors are defining ways to cut any “double-layer” through several make or buy (bundle / unbundle) decisions, especially when dealing with Packages. In this context of several uncertainties, there is a strong need for certainty for time and costs of any supply.

3. ESG Sustainability: End-Users and Financial Institutions (Bank, Insurance Co., …) demand specific requirements of the assessment of ESG Sustainability of the Supply Chain. The lack of a common International Guideline on how to assess ESG performance for Suppliers in Plant Engineering has been tackled since 2019 by ANIMP, through a collaborative approach – valid globally – and named “Supply Chain ESG Guideline”.

4. Carbon Emissions: Scope 3 carbon emissions account for more than 90% of the total emissions of any Buyer organization and the CO2 emissions of a Supplier are a new requirement, for joint estimate and collaboration. Compulsory funds for CO2 R&D are being defined globally to several industries to accelerate the achievement of CO2 neutrality. For example, the International Chamber of Shipping (ICS) proposed a $5 billion fund of mandatory R&D contributions from ship-owners globally. Finally, having a product or service portfolio to tackle CO2 reduction and removal is becoming of great worth.

5. Local Content: LC regulations differ from country to country, and it requires a tailored approach. Together with the funding by ECAs, LC is one the driver able to truly impact a Project Procurement Plan. In addition, a different type of Local Content after Covid-19 might rise in the near future: “nationalism” in industrial manufacturing.

6. Energy Transition: Investments in Green Hydrogen are still at an early stage ($90 Billion of Plant CAPEX in the period 2020-2023 vs $1.954 in traditional Oil&Gas) with many projects facing delays due to uncertain financing and complex JVs. On the contrary, the players that will have an early engagement on the Energy transition will be the ones benefiting the most from it.

7. Visibility and Supplier Engagement: Buyers that want to achieve CO2 neutrality need to engage and collaborate with suppliers to really reduce their emissions. The relationship with suppliers is crucial and visibility of Suppliers’ capabilities and traceability is a must. Key is also the transition from a “monitoring” model to a “feedback and reward” model.

8. Digital & Standardization: Collaboration is becoming a key in digital for standardization (e.g. the Catena-X initiative in the Automotive). An alliance for secure and standardized data exchange also in the Plant Engineering industry should be envisaged for the areas of quality management, logistics, maintenance, supply chain management and sustainability. It’s using technology to manage risks, not just financial but also reputational and sustainability related.

9. Project Management: Supply Chain will be a mix of global and local. Specs will be more standardized, support activities will be outsourced, and decisions will move faster. There is scarcity of essential project roles and Project Managers need new tools to support their decision making.

10. Industrial Politics: The industrial world has seen decades of stagnant productivity with limited planning and industrial politics directions. The lack of privileged Finance will be a growing issue and to sustain Suppliers’ growth in the coming years this trend must be reversed. A new digital “industrial district” of interconnected players with strong complementarity among players and shared digital infrastructure could support constant visibility & high-speed information also in the complex Supply Chains on Plant Engineering.

As said by Winston Churchill, the B2B industrial should “never let a good crisis go to waste” and the players that will better adapt and evolve around these 10 macro-trends will be the front-runner in the post-COVID re-start.

The full Report can be downloaded at the following link.